Big Deals Return

- China's 'serious' investments

- Soverign wealth funds expand in Asia

- Shopping in Italy

- More Chinese cash abroad, than at Home

- South Africa

- Foreign investors in the U.S. - 2014 - big year

- Coming in as Developers

- Ho hum...another one? New Jersey this time

With geopolitics so tenuous globally, the ca$h-rich Chinese saver is spreading their wings and playing global monopoly in cities where their children are being educated - like Vancouver, San Francisco and London.

China-based acquisitors are new to this game but have managed to make a big splash like China Anbang's purchase of the Waldorf Astoria in New York; Shanghai Greenland's purchase of Hertsmere site in Canary Wharf in London, and elsewhere.

Now they are trying second tiered cities like Seattle, Los Angeles, Sydney & Canberra, and Toronto. There is a new found confidence with these Chinese investors as their wealth has increased in the last decade and they are not shy to take on developments.

There is so much new wealth generated in the last ten years and a rising middle class which is the world's growing fastest consumer market.

Chinese Acquisitions

Chinese global cross-border acquisitions topped $54.3 billion this year, up 35 percent, Bloomberg available data show. Shanghai-based Fosun International Ltd. (656) in January outbid a U.S. buyout firm for Portugal’s 80 stake in Caixa Geral de Depositos SA’s insurance unit for 1 billion euros. Hong Kong-based Cosco Pacific Ltd. (1199) is among bidders of a state-fund stake in Piraeus Port Authority (PPA) while a Chinese venture is seeking a majority in Athens International Airport. -- 2014 October 12 BLOOMBERG

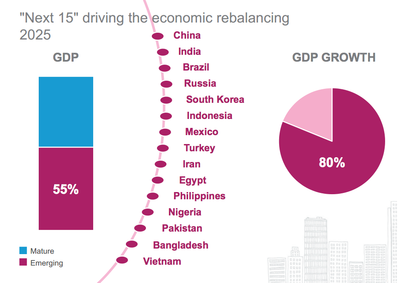

The “Next 15″ will drive 80pc of emerging market growth by 2025: report

July 30, 2014

Sixty percent of the world’s population live in the Next 15

As emerging markets continue to grow, 600 of the world’s top cities will be responsible for nearly 85 percent of global economic growth by 2025, according to a new report by McKinsey.

McKinsey suggests that through mass urbanization there will be 60 megacities, double that of today, accounting for a quarter of global GDP. To target these areas of growth, luxury brands must adjust strategies to include cities that may not yet be on their radar to ensure that they have a presence as new markets begin to flourish.

“It is hard for a brand entering a new emerging market to do everything at once,” said Sophie Marchessou, associate partner at the apparel, fashion & luxury group at McKinsey, New York.

“Resources are often time limited (management attention, investment available…), so it is better to have a disciplined approach to target in priority cities that matter most,” she said. “The largest cities in an emerging market also usually have a spillover effect on smaller cities, so by being present in the right cities, you improve your brand awareness overall.

“[Economic rebalancing] will affect [marketers] in many ways. There will be a constant conversation in companies about resource allocation, offer tailoring, brand building, etc.”

McKinsey’s LuxuryScope “The glittering power of cities for luxury growth” report used a methodology called CityScope that draws upon economic and socio-demographics for more than 2,600 cities around the world. McKinsey’s data goes down to the city level to predict growth and can be used by luxury brands to determine how to approach growth opportunities based on location.

Finding a city

For the first time since the Industrial Revolution, the world is undergoing a significant economic transformation. For example, modern-day China is urbanizing at a speed 10 times faster than the urbanization of 19th-century Britain, thus making Asia the world’s “economic center of gravity.”

Growth extends beyond China and the other BRICs to include what McKinsey calls the “Next 15.” These additional 11 countries are set to drive 80 percent of emerging market growth even though they only account for 25 percent of the global GDP.

These regions include South Korea, Indonesia, Mexico, Turkey, Iran, Egypt, the Philippines, Nigeria, Pakistan, Bangladesh and Vietnam. With 60 percent of the world’s population living within these countries, brands now have opportunities for growth outside the traditional established markets.

Although a significant amount of these emerging city markets are located in China, brands must extend their retail footprint within the Next 15’s smaller cities where growth potential is high. The 100 highest-growing cities such as Pune, India, Harbin, China and Luanda, Angola, will grow significantly in comparison to megacities such as Shanghai and Moscow.

McKinsey suggests that within the next 15 years the approximately 400 “second-tier” cities will yield wealth equivalent to the United States economy today.

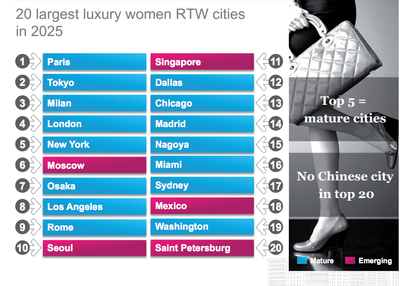

Though other cities are growing, this does not necessarily mean the irrelevance of established markets. In terms of women’s ready-to-wear in the 20 largest city markets in 2025, for example, no Chinese cities make the cut and no emerging market cities fall within the top 5.

Western mega cities will benefit from “riding the wave of growth” as emerging countries develop and their maintained status will be driven by “cultural fit” and factors determined by category and price point. This is especially true for women’s luxury ready-to-wear, dominated by established fashion capitals such as Paris, Milan and New York.

Growth in emerging market cities is already apparent in luxury sectors such as fashion, spirits and beauty. Research suggests that luxury women’s wear will grow from less than 10 percent a decade ago to 32 percent in 2025, while high-end beauty products will double to represent 47 percent.

McKinsey chart showing shift in emerging marekt categories

Although this growth signals that emerging markets are growing three times faster than their mature counterparts, moving into these areas is less advanced and will enable brands to make an impression much easier than they would in an established city.

Ninety percent of global luxury growth will result from consumers living in the top 20 apparel growth cities, seven of which are found in the Next 15 countries. China leads the way by driving half of this growth, while the remaining markets account for one-fifth of luxury consumers by 2025, a population four times that of the United Kingdom.

Growth spurt

McKinsey chart showing shift in emerging marekt categories

Although this growth signals that emerging markets are growing three times faster than their mature counterparts, moving into these areas is less advanced and will enable brands to make an impression much easier than they would in an established city.

Ninety percent of global luxury growth will result from consumers living in the top 20 apparel growth cities, seven of which are found in the Next 15 countries. China leads the way by driving half of this growth, while the remaining markets account for one-fifth of luxury consumers by 2025, a population four times that of the United Kingdom.

Growth spurt

To find success in these new market cities, McKinsey suggests a “city-by-city” strategy that allows brand to readjust business models, resource allocations and organizational structure. McKinsey sees this approach as a “compass for companies seeking to navigate the vast sea of emerging markets” whether in Belo Horizonte, Brazil or Wuhan, China.

Five main touchpoints should be tackled before a brand selects to enter an emerging city market. These include identifying the right go-to-market model per location, determining the need for local customization, ensuring standards in global customer service, gauging the need for organizational alterations and how to allocate resources.

These tactics have been undertaken by other brands that have entered emerging markets before the floodgates were opened, despite the risk.

For example, Estée Lauder Cos.’ expansion practices are marked by entering emerging markets ahead of other companies despite the increased risk, according to the “Building Empire” session May 13 at the FT Business of Luxury Summit.

Understanding risk tolerance is a must when embarking on any new project, especially when setting up shop in marketplace that is still developing. As one of the world’s most valuable brands, Estée Lauder strives to introduce its products ahead of competitors to better understand emerging markets (see story).

Beyond general market demographics, brands entering a new city location must have a handle on local culture, especially in the beauty sector.

For beauty marketers targeting consumers in emerging markets, it is essential to understand the grooming habits and preferred personal care products in the country at hand, according to a survey conducted by Euromonitor International.

In 2013, global sales of skin care products totaled more than $107 billion and the hair care market totaled $77 billion. These global sales figures, estimated to grow by 20 percent between 2014 and 2018, are reflective of the time, money and effort consumers spend on their appearances (see story).

Strategies must be outlined per country, rather than an oversweeping global tactic for all.

“The power of mega cities in the future,” Ms. Marchessou said. “Many cities will be as large as countries – Tianjin will be the size of Sweden, Shanghai will be the size of Poland and Portugal together.

“It varies slightly by category but for luxury women ready to wear for example, Moscow, Singapore, Mexico City, Seoul and St. Petersburg will be in the top 20 largest cities by size,” she said. “Beijing or Shanghai don’t make it to the top 20 but are among the fastest growing.

“What those cities share is a growing upper class that drives the purchase of luxury apparel and potentially some tourist spend [which is] usually more relevant for developed cities though.

Authors: Aimee Kim, partner at McKinsey’s Seoul office, Nathalie Remy, principal and co-leader of McKinsey’s apparel, fashion & luxury group, Jennifer Schmidt, partner and Leader of Americas’

apparel, fashion & luxury group at McKinsey, NJ and Benjamin Durand-Servoingt, engagement manager at McKinsey, Paris.

For the first time since the Industrial Revolution, the world is undergoing a significant economic transformation. For example, modern-day China is urbanizing at a speed 10 times faster than the urbanization of 19th-century Britain, thus making Asia the world’s “economic center of gravity.”

McKinsey chart showing shift in emerging marekt categories

McKinsey chart showing shift in emerging marekt categoriesTo find success in these new market cities, McKinsey suggests a “city-by-city” strategy that allows brand to readjust business models, resource allocations and organizational structure. McKinsey sees this approach as a “compass for companies seeking to navigate the vast sea of emerging markets” whether in Belo Horizonte, Brazil or Wuhan, China.

apparel, fashion & luxury group at McKinsey, NJ and Benjamin Durand-Servoingt, engagement manager at McKinsey, Paris.

PUBLISHED FEBRUARY 03, 2014

More firms venturing into overseas property

Australia, UK, US hot spots; US$3.5b invested abroad in first 9 months of last year

Firms have ramped up their geographical diversification efforts in recent months in a bid to escape Singapore's prohibitive property cooling measures -

[SINGAPORE] Firms have ramped up their geographical diversification efforts in recent months in a bid to escape Singapore's prohibitive property cooling measures. In the opening weeks of January alone, Aspial Corporation unveiled two acquisitions in Australia, Keppel Land agreed to purchase land in Indonesia and CapitaLand picked up yet another plot in China.

Australia, the United Kingdom and the United States have been firms' favourite hot spots. Several companies, including Hiap Hoe, AIMS AMP Capital Industrial Reit, Aspial, and Suntec Reit, picked Australia for their first overseas acquisitions.

Hiap Hoe, for instance, bought a 40,489-square-foot site in Melbourne, which it intends to develop into a 425-unit project, and then quickly went on to snap up a commercial building at 380 Lonsdale Street and a retail and office property at 206 Bourke Street. The three acquisitions cost the company about A$177.6 million (S$198.4 million). Aspial bought a freehold commercial building in Melbourne for A$41.5 million, soon followed by a separate commercial building also in Melbourne for $42.3 million. It intends to redevelop the latter site into what will be the tallest building in the city, subject to aviation clearance.

Among Reits, AMP Capital picked up a 49-per cent stake in Optus Centre, a business park in Sydney, for A$184.4 million, while Suntec Reit bought 177-199 Pacific Highway, a freehold land and property with a 31-storey Grade A commercial tower that is targeted for completion in early 2016. These were the first overseas acquisitions for both Reits.

Andrew Bird, chief investment officer (property) at AMP Capital, said he expected investment interest in Australian property to continue to remain high, particularly for the office and residential sector.

"The attraction of Australia (lies in its) high yield relative to other markets globally," said Mr Bird, noting that yields for prime property in Australia are about 6 per cent.

"When global investors look at property markets on a relative basis, they look at Australia and they see the high starting yield. And while the economy has softened a bit - the mining boom has slowed down - we are still looking at GDP growth of about 2.5 to 3 per cent," said Mr Bird.

The above two factors, plus sustained population growth through organic growth and immigration, are reasons why interest in Australia will likely remain high. That developers are looking elsewhere is perhaps not surprising, given plunging sales at home.

"New and adjusted local government policies in recent years that were meant to prevent a real estate asset bubble from forming and bursting, have, somewhat, limited the opportunities here for investors and developers," noted Chia Siew Chuin, director for research and advisory at Colliers International. "In addition, the property playing field in Singapore has matured with many players bringing more diversity into the game, hence increasing the level of competition," she said.

According to data released by DTZ, close to US$3.5 billion was invested overseas by Singapore-based investors in the first nine months of 2013.

Notably, this figure does not take into account GIC's 50 per cent stake in London's Broadgate business district, a retail and commercial estate of 17 office buildings. While the consideration for GIC's purchase was not disclosed, reports placed the price tag at around £1.7 billion (S$3.56 billion) - believed to be a record for a central London property.

London has emerged a popular investment spot thanks to its reputation as a stable financial centre, said CBRE's Chris Brooke, executive managing director for Asia.

"Asian developers buying institutional Grade A office assets in London are driven by the feeling that London is a stable financial centre, offers reasonable yield, and is a long-term core holding. There is also the desire to have a flagship property in London," said Mr Brooke.

"(On the residential front) it is a good market to be building high quality residential homes notwithstanding the capital gains tax. The feeling is that demand will remain, even though it may trail off a little bit," he added.

City Developments Limited (CDL) and Oxley Holdings are among the firms that made forays into the London market in the last 12 months - CDL via a freehold plot near Harrods in Knightsbridge, which it intends to redevelop, and Oxley Holdings via a mixed development site at London's Royal Wharf.

Other firms also entered the fray. Local construction group Lum Chang added a London hotel near the tourist attractions of Hyde Park and Kensington Gardens to its growing list of London properties last year.

Property in the US also received its fair share of interest. SingHaiyi group - previously known as SingXpress Land - snapped up two distressed commercial projects in the US in the last few months, after Neil Bush, the brother of former US president George W Bush, was brought on board as non-executive chairman of SingHaiyi.

The two projects, Tri-County Mall in Ohio and Vietnam Town in California, were picked up for US$45 million and US$33.1 million respectively. Earlier this month, the group said that it is in talks to acquire another two to three assets in America.

Separately, OUE picked up California's tallest building - the US Bank Tower in Los Angeles - for US$367.5 million, while earlier this year GIC sealed a deal to buy office space in New York's Time Warner Centre with two partners, the Abu Dhabi Investment Authority and US real estate firm Related Companies, for US$1.3 billion.

While many local firms have been acquiring plots overseas, one of the most active is local developer Oxley Holdings, which now has ventures in Malaysia, Cambodia and China.

Following its first move abroad in May last year, in which it bought a firm with rights to a mixed-use site in Kuala Lumpur, Oxley Holdings has assembled an impressive portfolio of plots through a combination of joint ventures, development right agreements and acquisitions.

In January, the group said it signed a framework agreement with Sepang Goldcoast and Sepang Bay to develop land. The latter two hold interests in two parcels of 99-year-leasehold land with an aggregate area of about 47.3 hectares in Sepang. The joint-venture agreements entitle Oxley Treasure to 85 per cent of the gross development value of the developments on the land.

As to the future for acquisitions, some experts urge caution as the global economic recovery proceeds.

Speaking on the sidelines of the DTZ Annual Property Outlook Seminar 2014 earlier this month, Dominic Brown, head of South East Asia/Australia and New Zealand Research, said: "From an investment perspective, the main point is that (globally) property is not expected to get any more attractive on a relative value basis in the near term ... This stems from the fact that upside risks are now increasingly likely as the global economic recovery starts to gather momentum. This is a big shift from last year when a lot of focus was on what might happen if the eurozone broke up."

- Developers flock to Asia with their projects

- Princelings

- Cloning HKG developments and global tenants in SHA

- Asia Institutional Investors

- Hong Kong investors amongst most sophisticated

- Asian institutional investors buy big globally

- Canadian Retail Players Now Continental

- Wanted: China Property Agents

- Vancouver Canada - the Geneva of the Asia Pacific

- Asia's Richest Billionaire is Selling

- London is on fire

- The Chinese Are Everywhere - in Property - its a Hobby!

- What to buy today?

- Our favourite Asian property stock

No comments:

Post a Comment